3 Key Points in PMK 66/2023 on Natura Tax Treatment

In the terms of taxation, the treatment of non-cash income is crucial to be clearly understood and regulated. One type of tax that governs non-cash income is the Natura Income Tax (NIT). Natura Tax has been detailedly regulated through the Minister of Finance Regulation (PMK) Number 66 of 2023.

This PMK provides important guidelines in determining how income in the form of goods or services should be fairly and transparently taxed. In this article, TGS AU Partners will provide a detailed explanation of the 3 main points outlined in PMK 66/2023.

Understanding What Natura Tax is

Natura Tax is a tax imposed on employees who receive income in the form of goods or facilities provided by the company. Previously, income types such as vehicle facilities, allowances, commissions, and bonuses were not subject to tax. However, with the issuance of PMK 66/2023, these incomes have now become the subject of Natura Tax.

One of the main objectives of the Natura Tax policy is to address tax avoidance practices by companies through providing facilities to employees. With the implementation of the Natura Tax, companies are expected to be more compliant in fulfilling their tax obligations related to non-monetary income.

Background of Regulation PMK 66/2023

The issuance of Minister of Finance Regulation (PMK) Number 66 of 2023 regarding the treatment of Natura Tax is based on several relevant factors and considerations. The following are some of the backgrounds that underlie the issuance of this regulation:

- Tax avoidance: One of the main factors is the practice of tax avoidance by some companies. Some companies attempt to reduce their tax obligations by providing income to employees in the form of goods or facilities, rather than monetary compensation. This results in such income not being taxed as it should be. To regulate this practice, the government needs to establish tax treatment for non-monetary income.

- Tax fairness: The issuance of PMK 66/2023 is also motivated by the desire to create fairness in the taxation system. Fair and equitable taxation is important to ensure that all types of income, whether received in the form of money or non-monetary compensation, are subject to tax in proportion to their value. With the Natura Tax policy, non-monetary income will also be subject to taxation based on its fair value.

- Tax compliance: The government aims to encourage companies and individuals to comply with their tax obligations. With the implementation of PMK 66/2023, companies are expected to be more compliant in fulfilling their tax obligations related to non-monetary income. This can also encourage companies to be more transparent in reporting employee income and ensure that the Natura Tax is accurately paid.

Considering these factors, the government issued PMK Number 66 of 2023 as an effort to provide clear guidelines in the treatment of Natura Tax. The goal is to enforce tax fairness, prevent tax avoidance, and promote tax compliance. With the implementation of this regulation, it is expected to establish a more transparent, fair, and accountable taxation system.

Furthermore, Dimas Emha Amir Fikri Anas, SE., M.SA., CA., CPA, as the Audit & Assurance Partner of TGS AU Partners Malang branch, believes that the implementation of the latest tax regulations regarding natural resources is expected to provide companies with confidence in enhancing employee welfare through specific facilities that can be legitimately deducted as tax-deductible expenses in accordance with tax regulations.

3 Key Points in PMK 66/2023 on Natura Tax Treatment

Minister of Finance Regulation (PMK) Number 66 of 2023 regarding the treatment of Natura Tax regulates various aspects related to the taxation of income in the form of natura. Here are the 3 main points outlined in this PMK:

Reimbursement or Compensation in the Form of Natura Resources

In PMK 66/2023, one of the main points addressed is the treatment of reimbursement or compensation in the form of natura. Previously, income received in the form of natura often went untaxed, allowing companies to use this method to avoid tax obligations by providing facilities to employees. However, with the introduction of PMK 66/2023, income in the form of natura must be taken into account and subject to taxation based on its fair value.

The purpose of this treatment is to create fairness within the taxation system and prevent tax avoidance practices by companies. By imposing taxes on income received in the form of natura, it is expected that companies will be more compliant in fulfilling their natura tax obligations and no longer utilize non-monetary facilities as a means to reduce their tax liabilities.

In practice, companies are required to calculate the value of natura provided to employees and treat it as taxable income. Taxes will then be levied on the value of the natura in accordance with the prevailing tax rates. With the implementation of this treatment, the aim is to achieve transparency, fairness, and compliance in the taxation of non-monetary income.

List of Natura Resources as Taxable Objects and Exemptions

This list explains the types of goods and services that can be received as income in the form of natura and will be subject to taxation. For example, housing facilities, motor vehicles, electronic goods, travel expenses, or concert tickets received by employees as part of their compensation package.

However, within PMK 66/2023, there are also specific exceptions. These exceptions define certain types of natura that are not subject to taxation. This may be related to specific conditions or limitations set by regulations. For instance, there may be exceptions for natura with a value that does not exceed a certain predetermined amount, or natura provided for specific purposes such as emergency assistance or natural disaster relief.

This point is crucial for companies and employees to understand, as it can impact the tax obligations related to income in the form of natura. Companies need to understand the types of natura that are subject to tax and adhere to the applicable regulations. Similarly, employees need to be aware of their rights and obligations regarding the income they receive in the form of natura tax.

Procedure for Calculating Natura Resources as Taxable Objects

The calculation procedure for natura typically involves determining the fair value of the goods or services provided. Fair value is the value that can be reasonably obtained in an open market transaction between parties with no relationship between them. Companies must conduct objective and fair assessments to determine the fair value of the natura provided to employees.

Once the fair value is determined, it will be considered as income and subject to taxation according to the applicable tax rates. The tax imposed on natura income will be calculated based on the tax rates established by the prevailing tax regulations. Here is an example of how to calculate natura resources as taxable objects.

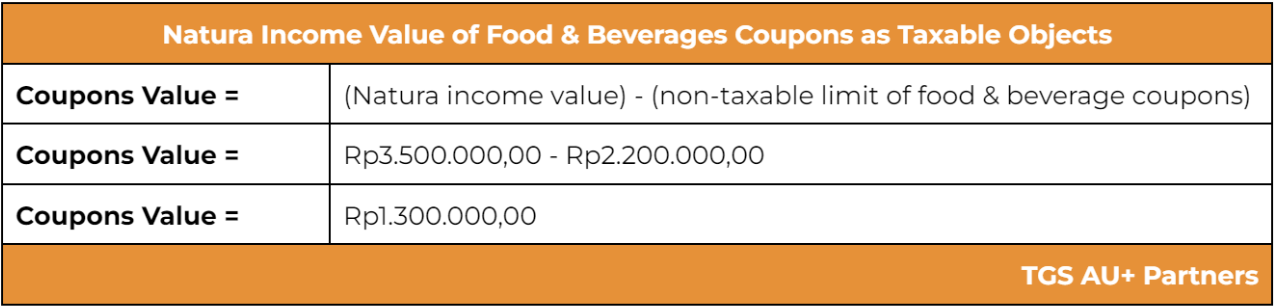

PT Wijaya provides food and beverage allowances to all of its employees in the office, amounting to Rp1,800,000 per employee per month. Additionally, employees in the marketing division receive an additional coupon value of Rp3,500,000 per employee per month due to their higher mobility outside the office. How much is the total taxable value of the food and beverage allowances in the form of coupons?

According to the latest regulation, the non-taxable limit for food and beverage allowances is Rp2,200,000 per month. Meanwhile, the coupon value received by employees in the marketing division of PT Wijaya is Rp3,500,000 per month. Therefore, there is a difference between the specific value limit and the value of the food and beverage coupons. Here is the calculation.

Thus, the taxable value of the coupon for natural resources is Rp1,300,000. Since the deduction of Natural Resources Income Tax (PPh Natura) is carried out through the mechanism of Article 21 Income Tax, the taxable value of Rp1,300,000 for natural resources will be included in the gross income of the respective employee.

Conclusion

In conclusion, Minister of Finance Regulation (PMK) Number 66 of 2023 regarding the treatment of Natura Tax plays an important role in regulating the taxation of non-monetary income. With these guidelines in place, the aim is to establish fairness in the taxation of income received in the form of goods or services.

Furthermore, by understanding the key points outlined in this PMK, whether regarding the reimbursement or compensation in the form of natura, the list of natura included in the Natura Tax, or the calculation procedure for natura, we can gain a better understanding of this type of tax and ensure its proper implementation.

News & Articles Recommendations.