Differences in Financial Statement Presentation between General Financial Accounting Standards (SAK Umum) and International Financial Reporting Standards (IFRS)

In managing financial reports within a company, accountants have guidelines or references known as Financial Accounting Standards (PSAK). These standards used are based on international accounting standards known as IFRS or International Financial Reporting Standards. In this article, TGS AU Partners will discuss more about the differences between IFRS and PSAK as well as their implementation in Indonesia.

According to Dimas Emha Amir Fikri Anas, SE., M.SA., CA., CPA (Partner Audit & Assurance at TGS AU Partners Malang Branch), stepping together with IFRS-based SAK can help open the door to business success in the global market. Transparency, easy comparability, and investor confidence form a strong foundation for achieving long-term success.

Implementation of General Financial Accounting Standards (SAK Umum) in Indonesia According to PSAK

Pernyataan Standar Akuntansi Keuangan (PSAK) is a framework for preparing company financial statements issued by the Indonesian Institute of Accountants (IAI). PSAK encompasses various rules for recording, preparation, execution, and presentation of financial statements.

PSAK is a system designed to regulate the majority of financial statement presentations, ensuring consistency in both conceptual and technical aspects. Consequently, PSAK has become an unquestionable standard for financial accounting and is widely used by almost all companies in Indonesia. Adhering to PSAK enables accountants to create uniformity in the presentation of financial statements.

Currently, several types of SAK are in effect in Indonesia, adopted by various entities including government institutions and private companies. The following are the five types of SAK:

-

PSAK-IFRS: Used by entities with accounting, such as publicly listed companies, insurance, banking, state-owned enterprises (BUMN), and pension funds.

-

SAK-ETAP: Used for entities with no significant public accountability, where financial statements serve general external users' purposes.

-

SAK-EP: Indonesian financial reporting standard for Private Entities, adopted from IFRS for SMEs while considering the conditions in Indonesia. SAK-EP will replace the Financial Accounting Standards for Entities Without Public Accountability (ETAP) and will be effective from January 1, 2025.

-

SAK-EMKM: Based on Law No. 20/2008, this SAK is used by entities or businesses that do not meet SAK-ETAP requirements.

-

PSAK-Syariah: SAK established by the Sharia Accounting Standards Board, used by institutions or businesses with Sharia policies.

-

SAP: Referring to Government Regulation No. 71/2010, this SAK is used by government entities for preparing Central Government Financial Statements (LKPP) or Regional Government Financial Statements (LKPD).

How is IFRS Applied in Indonesia?

Apart from SAK, Indonesia also implements international accounting standards known as IFRS (International Financial Accounting Standard). In essence, IFRS and General Financial Accounting Standards (SAK Umum) are not vastly different. IFRS also provides guidance and procedures for presenting a company's financial statements, but it is based on international standards.

IFRS is an international accounting standard published by the International Accounting Standards Board (IASB). It is formulated by four major global organizations, namely the International Accounting Standards Board (IASB), the European Commission (EC), the International Organization of Securities Commissions (IOSCO), and the International Federation of Accountants (IFAC).

As a member of the IFAC, Indonesia has adopted IFRS as one of its accounting standards. The implementation of this international accounting standard in Indonesia began in 2012. The government has made it mandatory for certain institutions, such as banks, insurance companies, publicly listed companies, and state-owned enterprises (BUMN), to use the IFRS system. Since these institutions are closely related to the public, using IFRS helps provide relevant information for users to read and analyze their financial statements.

Additionally, the application of IFRS in your company can yield various benefits, including:

-

Enhancing comparability of financial statements and providing high-quality financial information in the International Capital Market.

-

Removing barriers to international capital flows by reducing differences in financial reporting regulations.

-

Reducing costs for multinational companies in financial reporting and financial analysis for financial analysts.

-

Improving the quality of your company's financial reporting, moving toward best practices.

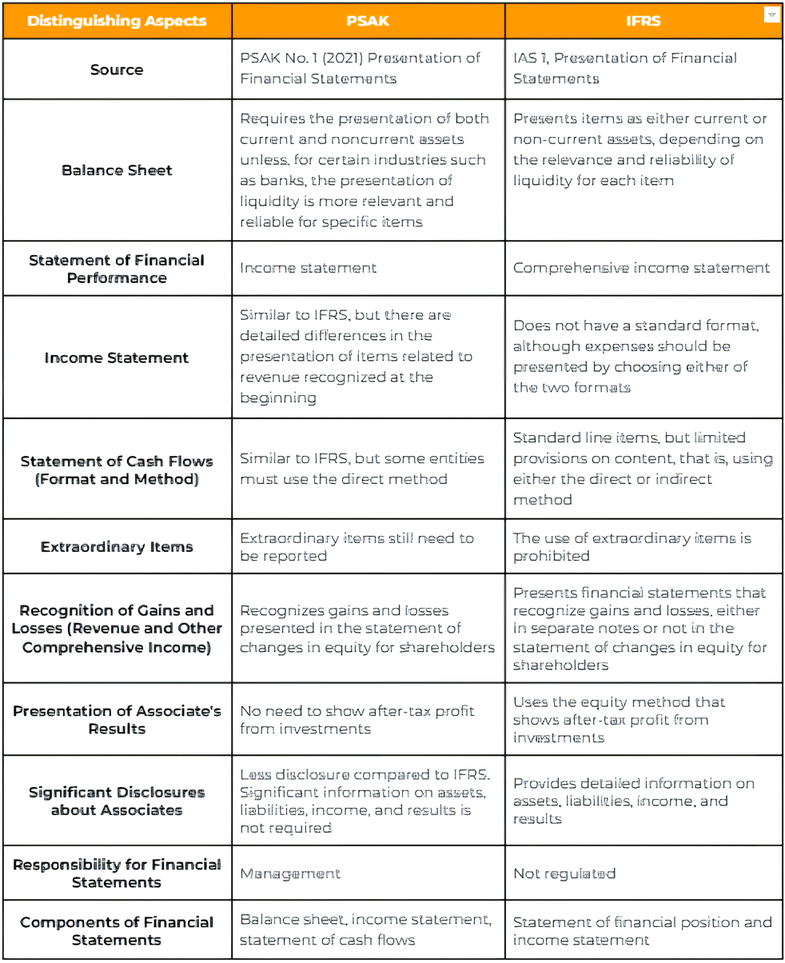

Table of Differences in Financial Statements between General Financial Accounting Standards (SAK Umum) and International Financial Reporting Standards (IFRS)

Below is a table comparing the differences between general Indonesian Financial Accounting Standards (PSAK) and International Financial Reporting Standards (IFRS) based on specific aspects.

Conclusion

Based on the description above, it can be concluded that both General Financial Accounting Standards (SAK Umum) and International Financial Reporting Standards (IFRS) are essential accounting standards to be applied in financial reporting, not only in Indonesia but also in the business world. By using PSAK and IFRS, companies can prepare financial statements more efficiently and rapidly, resulting in higher-quality reports.

News & Articles Recommendations.