5 Types of VAT at Certain Amount According to PMK 71/2022

Under the changes in the Harmonization of Tax Regulations Law, there are three mechanisms for calculating Value Added Tax (VAT): the general mechanism, calculation based on other valuation bases, and VAT at certain amount. One of the regulations that discusses a certain amount of Value Added Tax is PMK 71/2022.

This PMK governs five types of Taxable Services subject to VAT at certain amount. So, what are these service types, and what are the applicable rates and valuation bases? TGS AU Partners will delve into that!

The Issuance of PMK 71/2022

PMK 71/2022 was issued to regulate VAT at certain amount to provide ease, fairness, and legal certainty in collecting Value Added Tax on certain Taxable Services. This PMK is an implementing regulation of the provisions of Article 16G letter i of Law No. 8 of 1983, which was last amended to Law No. 7 of 2021 concerning the Harmonization of Tax Regulations.

Furthermore, the regulation, effective from April 1, 2022, is an adjustment to the provisions stipulated in:

-

PMK No. 75/PMK.03/2010 concerning Other Valuation as the Basis for Taxation, as last amended by PMK No. 121/PMK.03/2015;

-

Article 8 of PMK No. 92/PMK.02/2020 concerning Criteria and/or Details of Religious Services Exempted from Value Added Tax (PMK 92/2020);

-

Article 13 paragraph (5) letter b and Article 16 paragraph (4) letter b of PMK No. 6/PMK.03/2021 concerning the Calculation and Collection of Value Added Tax and Income Tax on the Transfer/Income related to the Sale of Credit, SIM Cards, Tokens, and Vouchers (PMK 6/2021).

Understanding What Is Meant by VAT at Certain Amount

VAT at certain amount is a specific VAT imposition mechanism for certain supplies carried out by Taxable Entrepreneurs (PKP). The criteria for PKP in this context are having a business turnover not exceeding a certain amount in a fiscal year, engaging in specific business activities, and/or making supplies of certain Taxable Goods or Taxable Services.

Provisions regarding business turnover amount, types of business activities, and types of Taxable Goods or Taxable Services are further determined by the Minister of Finance through a Minister of Finance Regulation (PMK). Until now, several PMKs have been established that regulate VAT at certain amount, including the following:

-

PMK Number 61 of 2022 concerning VAT at Certain Amount on Self-Construction Activities.

-

PMK Number 62 of 2022 concerning VAT at Certain Amount on Certain LPG Supplies.

-

PMK Number 64 of 2022 concerning VAT at Certain Amount on Certain Agricultural Products.

-

PMK Number 71 of 2022 concerning VAT at Certain Amount on Certain Taxable Services.

5 Types of VAT at Certain Amount

Referring to Article 2 paragraph (1) of VAT due at a certain amount. The specific Taxable Services mentioned in this article include:

-

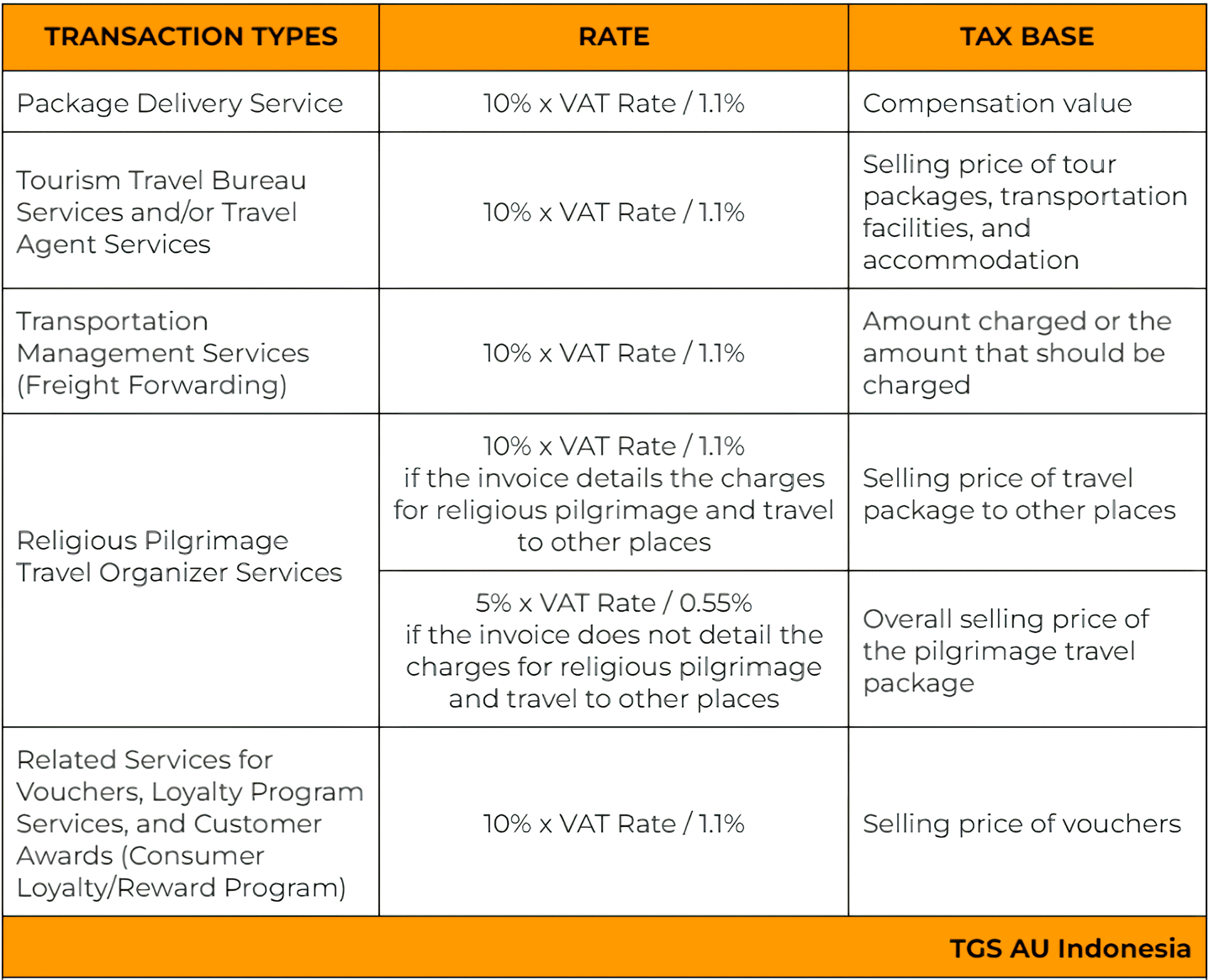

Package delivery services according to the regulations in the postal sector;

-

Tourism travel bureau services and/or travel agent services in the form of tour packages, transportation reservation, and accommodation reservation, where the supply is not based on the provision of commission/reward for intermediary sales services;

-

Transportation management services (freight forwarding) which include transportation charges in the service invoice;

-

Religious pilgrimage travel organizer services that also organize travel to other places; and

-

Organizer services in the form of voucher marketing; payment transaction services related to voucher distribution; and loyalty and customer reward programs (consumer loyalty/reward program), where the supply is not based on commission and no difference (margin) exists.

These five types of services are subject to VAT at a certain amount upon supply. This certain amount encompasses different tax rates and different bases of assessment. Below are the detailed rates and assessment bases for these five Taxable Services subject to VAT at certain amount.

For Taxable Entrepreneurs wishing to provide the five aforementioned Taxable Services, it is required to issue a tax invoice with transaction code 05. According to Article 5 of PMK 71/2022, entrepreneurs conducting the supply of the five mentioned Taxable Services are not allowed to credit input tax on the acquisition of Taxable Goods and/or Taxable Services, the import of Taxable Goods, as well as the utilization of intangible Taxable Goods and/or the utilization of Taxable Services from outside the customs territory within the customs territory, related to the supply of these five types of Taxable Services.

Conclusion

Based on the above discussion, it can be concluded that VAT at certain amount is one of the mechanisms for imposing VAT that is specifically used for certain supplies carried out by Taxable Entrepreneurs. Referring to PMK 71/2022, Taxable Entrepreneurs are required to collect VAT at certain amount on the supply of certain Taxable Services falling within the 5 specified categories based on the prevailing regulations.

VAT at certain amount is not just a new mechanism in VAT calculation but also a new regulation that can provide fairness for Taxable Entrepreneurs with low business turnover or engaged in specific business activities that do not benefit from VAT. Furthermore, the implementation of this mechanism can also stimulate economic growth and societal well-being through tax incentives for specific sectors.

News & Articles Recommendations.